Western Investment – Thesis Summary

Western Investment (WI) is a Canadian serial acquirer of small, niche, orphaned, profitable insurance carrier assets that they acquire close to book value. The two founders have separately (and prior to WI) built two of the largest insurance operations in Canada through serial acquisitions. They have the vast majority of their net worth invested in company stock.

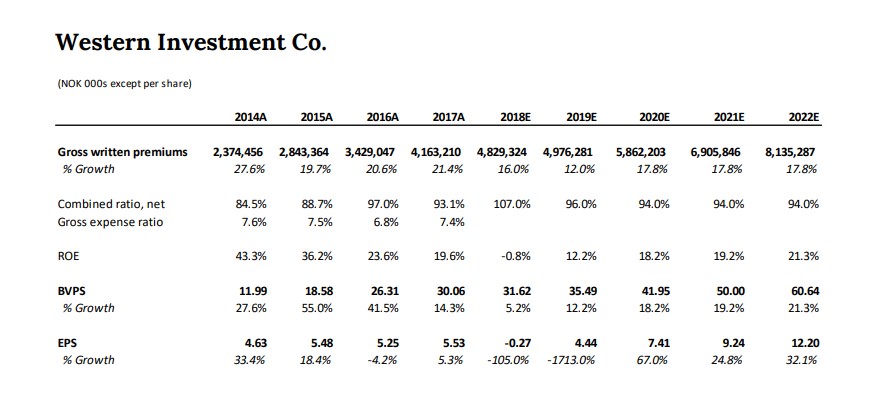

WI’s small starting size will allow it to compound BVPS at high rates for over a decade. The transaction is structured very attractively, essentially allowing us to buy a business compounding BVPS ~25% at half of book value in a “two for one” deal.

Valuation

- Market cap = CAD 12.7mm = $9.4mm.

- Stock trades at 1x trailing book value, but in this transaction we would be purchasing at essentially 50% of book value.

- 10-year base case: 27% BVPS CAGR and an exit multiple of 2x book yield a 10-year net IRR of 33.9% (net MOIC of 18.5x) on our common shares (holding period Years 1-10) and a 5-year net IRR of 73.7% (net MOIC of 15.8x) on our warrants (holding period Years 6-10, as the warrants would be exercised at the end of Year 5).

- 5-year base case: 15% BVPS CAGR and an exit multiple of 1.5x book yield a 5-year net IRR of 34.5% and a net MOIC of 4.4x.

- To achieve our hurdle of a 20% net IRR over five years is not a heavy lift: 5% BVPS CAGR and an exit multiple of 1.5x book value or 13.5% BVPS CAGR and an exit multiple of 1x, for instance.

Both of these scenarios are possible solely through intelligent float investing. Western’s best comparable, Trisura, trades on average around 3x book value. If WI traded at 3x in five years, our net IRR would be 57% and net MOIC would be 9.5x. Large Canadian insurers have historically traded at 2-3x trailing book value and earned mid-teens ROEs. Historically, US insurers have earned an average ROE of ~10%, and have tended to trade around 1.3x trailing book value.

Business Description

Western Investment (WI) began as a private equity investment vehicle for co-founder Scott Tannas after his tenure at Western Financial Group. WI acquired stakes in three private businesses in Western Canada, and then took a 15% stake in a bootstrapped insurance carrier (Fortress Insurance).

Fortress has been very successful, growing to $30mm in annual premiums from scratch (founded five years ago) with excellent reinsurance relationships and operating profitably. It currently sells 100% short tail policies and the book is 85% property (60% commercial property). It plans to add a specialized auto line with 3-5 year policies.

Paul Rivett approached Scott and WI with the idea of divesting the three non-insurance private businesses and growing 1) Fortress and 2) through a serial acquisition strategy of small insurance carriers in Canada, and operating them in a decentralized manner with centralized capital allocation (the Berkshire Hathaway model). We consider Paul a co-founder of the “new Western Investment Co” along with Scott. The three non-insurance businesses are likely to be divested so we won’t spend time on them here. They are Glass Masters, Foothills Creamery, and Golden Health Care.

Transaction Particulars

WI is raising ~$37mm of capital through a private placement and rights offering to existing shareholders. This capital will be used to put Paul’s plan into motion: to acquire 100% of Fortress (the deal has already been agreed and will conclude at the same time as the capital raise) at a pro forma book value of $18.2mm, as well as to begin acquiring other small, niche insurance carriers.

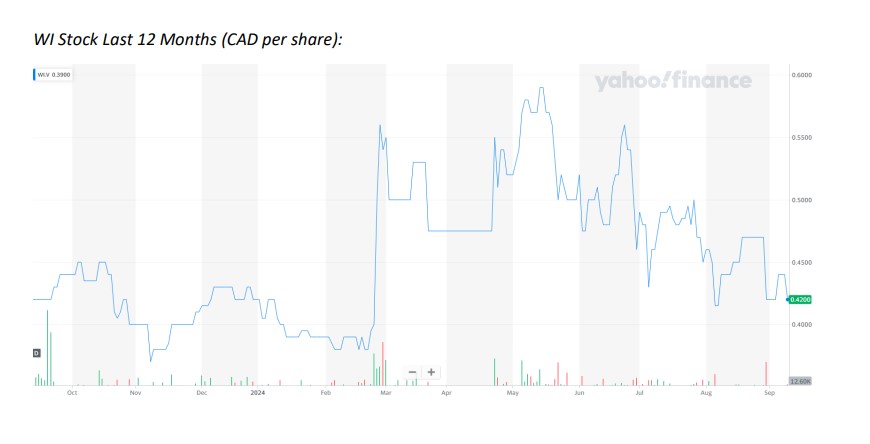

The private placement, in which we are participating, offers extremely attractive terms: each private placement Unit costs $0.40 and provides one common share of WI and one 5-year warrant exercisable at $0.47 (the current stock price is $0.42). The book value per share of WI after the transaction will be ~$0.43. Thus the private placement provides us with one share at less than book value, along with a 5-year warrant for free. It is essentially a two-for-one deal, and means we are purchasing at ~50% of book value.

The warrant structure allows us to put down no capital for the second of our two shares in each Unit, meaning that any increase above $0.47 five years from now would provide pure profit to us with no need to put down any principal. This dynamic contributes significantly to the very high base case IRR.

Management

Paul Rivett (54), one of the co-founders, is a value investor who was formerly the President of Fairfax Financial, part of the Canadian P&C insurance oligopoly. He reported to founder and Chairman Prem Watsa. As President of Fairfax, Paul made and managed many acquisitions of small insurance carriers. Eventually, however, he came to believe that Prem Watsa’s approach of buying “cigar butts” was inferior to buying good businesses at a good price. He retired from Fairfax and began searching for an insurance company he could acquire and grow and where he could improve float investments. Paul is building a culture that relentlessly focuses on measurement, speed/nimbleness, and frugality.

Scott Tannas (62), the other co-founder, founded Western Financial Group in 1993 when he was 31. He built it, through acquisitions and organic growth, into the largest insurance broker in Western Canada by the early 2000s. Between Paul and Scott, they have extensive experience and an excellent understanding of the Canadian insurance market and how to generate high ROEs through underwriting and smart float investing.

Shafeen Mawani is the CEO of Fortress. He is an actuary by training, an entrepreneur, and is very proud of successfully bootstrapping Fortress over the last five years. He strikes us as ambitious and certain of Fortress’s ability to grow its premium base.

Capital Allocation & Incentives

Paul will own just below 20% and that equates to a significant portion of his wealth. Scott also has a significant portion of his wealth in WI stock, and Shafeen owns 10% of Fortress.

Management engages in a rigorous analytical process around capital allocation, determining which opportunities offer the highest long-term returns. They refuse to acquire insurance operations that they can’t operate at a better than 95% combined ratio, and thus at higher than 20% ROEs. They plan to make acquisitions at 1.5x book value or less, with a significant portion of them at or below book value. WI will continue paying a small dividend (CAD ~150K) until the shareholder base turns over.

Duration of Growth & Incremental Returns

WI believes it can significantly grow premiums and fee revenue by acquiring small insurance companies under a serial acquirer model. Paul and Scott have built an M&A pipeline that includes 100 current opportunities. They believe there are ~15 different types of “mouse traps” that they can purchase around book value and that will earn better than 95% combined ratios.

As for WI’s existing insurer, Fortress, the plan is to grow premiums to $100mm in 2028. Fortress’s true claims ratio has been in the exceptional range of 30-40% of premiums. Shafeen will achieve his $100mm GWP target through continuing to increase Fortress’s participation in the MGA (managing general agents) market in Canada, growing their fronting business, and utilizing reinsurance.

WI’s model is to acquire commercial specialty insurance carriers with better than 95% combined ratios and 2x-3x premiums/equity leverage, yielding a range of 10% – 24% ROEs just from underwriting. By adding the underwriting and float investment ROEs together, we discern the ROE of the entire WI business can comfortably reach between 20% and 48%. We believe normalized ROE and BVPS will be 25%-30%.

Competitive Moat

The industry structure of the Canadian market is attractive, with an oligopoly of a few large players, no mid-sized players, and then a long tail of small players. The large players earn mid-teens ROEs, while many of the niche, small insurers earn ROEs above 20%. This compares to a far more fragmented market in the US, with the top three players accounting for 20% of premiums, which has led to an average 104% combined ratio and ROE ~11%. This industry structure came about from consolidation: the large players acquired all the mid-sized players. The small players either operate in niches that are too small to matter to the large players (and hence earn >20% ROEs), or they are subscale and can’t compete. Because there are no mid-sized players, as we mentioned above, and also because PE firms don’t want the regulatory hassle and licenses to participate, there are many small, attractive orphaned assets. This is WI’s advantage: they are the only buyer for these opportunities, due to market structure.

Barriers to Entry

At the same time, barriers to entry on two levels are high: one, it is impossible for a startup to get an insurance license from the regulators. In addition, even for large foreign insurers it takes significant capital and three years to get a license. Two, there are barriers to success in being successful at WI’s strategy of acquiring attractive opportunities. These opportunities are not necessarily easy to identify; Paul, Scott and Shafeen hear about them through their extensive networks, and their pattern recognition allows them to sift quickly through which ones are promising and which are landmines. This may sound simple but it is essential. There are plenty of landmines in the insurance space, and avoiding those is job #1. The deals are complex to the layperson. There is tight regulatory supervision. Paul and Scott, especially, have this expertise from their many years of small acquisitions. This is certainly not a space in which a 32-year-old Harvard MBA who has never worked in the industry could be successful, like many other serial acquisition and search fund spaces (VMS, etc). As WI gains a reputation for being a home for orphaned assets, their ability to identify and close deals will only grow. In niche insurance markets, underwriting expertise and relationships are what matter. Paul and Scott have these in spades. In addition, Shafeen has built an excellent reputation for Fortress in its niche, such that at only $30mm of premium, they have seven rated insurers in their reinsurance stack and they grew premiums above 100% last year.

Independent Broker Advantage

Another advantage that WI has in today’s Canadian market is that independent brokers (not the large few) have a problem that there are no longer any mid-sized insurers in Canada. Many of them may have only three markets or products they’re in, and they depend on the few large insurers for business. But those insurers have in-house brokers, and this channel conflict can mean that the insurer could call up the independent brokers and say “we’re cutting you out of this market and giving it all to our brokers so they can put our capital to work.” In that case, a broker can lose a third of his/her business. The independent brokers want to diversify to smaller insurers for this reason, and they work to support up and coming insurers like WI and Fortress. They want more mid-sized insurers to appear.

Underwriting Discipline

WI also focuses intently on underwriting discipline. In insurance in the US, you frequently see companies writing unprofitable business during soft (low-price) markets. There will be no incentives for underwriters at WI tied to premium growth, and instead incentives will be tied to a combined ratio target with a three-year look back (to ensure reserves develop favorably). Paul talks continually of how they will build WI’s culture to be focused on not writing unprofitable business. As he says, he’d rather his underwriters and brokers go golf instead of write unprofitable business.

Analogs

Trisura

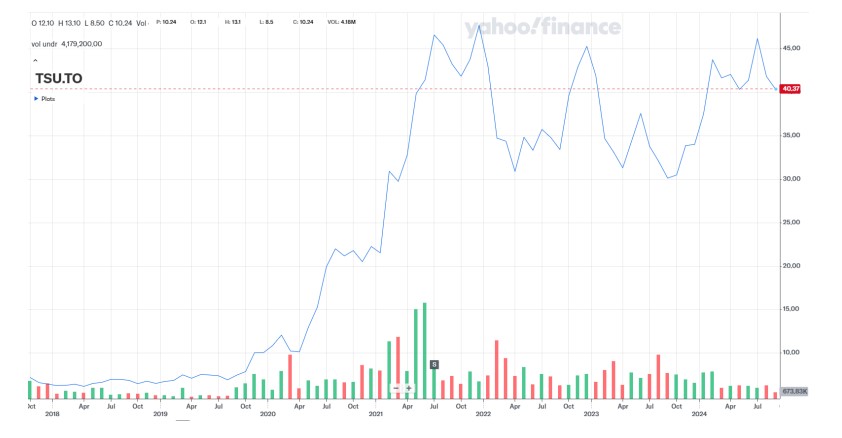

Trisura, when it was getting started, took a similar approach to Fortress. They grew from nothing within Brookfield and then spun out in 2017. They grew by focusing on fronting (a key for Fortress), and that is still 50% of their premium, and by engaging in small M&A. They used a lot of reinsurance in the beginning as well, just as Fortress does. Now Trisura have $1bn in premium and trade around 3x book value. They don’t do as much M&A now because the opportunities no longer move the needle for them, and there are no mid-sized players to acquire. A key difference between Trisura and WI is that Trisura has a much lower ROE hurdle rate for investing in new projects (15%), which led to them issuing a lot of equity in the early years (Paul and Scott do not want to issue equity again, they’d rather utilize debt and reinsurance to fund capital needs). Ultimately, they have still compounded BVPS at 20% over time, and their stock has followed suit. We believe WI has the opportunity to beat Trisura’s outcome (5.5x MOIC in six years, or a 33% IRR).

Fairfax

We have already discussed Fairfax’s long term value creation. The company grew through serial acquisition of small insurers in its early years, when most of its BVPS and stock price growth occurred. Fairfax has engaged in larger acquisitions of late, including ones outside of Canada. As we mentioned previously, they also tend to purchase underperforming insurance assets at cheap prices (70-80% of book value), which is not what WI intends to do. Yet there are more similarities, such as running a decentralized operating structure (high autonomy at each of the insurance subsidiaries) and seeing the float as a large value creation lever (which most insurance companies don’t do).

Western Financial Group

As we described above, Scott Tannas grew Western Financial through serial acquisition of small insurance brokers. He also bought a life insurance company and a bank, both yielding successful outcomes. He utilized the same approach to relationship building as he will at WI. However, the key difference with WI is that WI will typically acquire carriers, not brokers.

Enstar Group

Enstar has done 100+ acquisitions / books of business transactions since their founding. They acquire insurance lines that other carriers have placed into runoff. Enstar did exceptionally well in their first decade after IPO from 1997 to 2007 (up ~1,400%) but not as well in their most recent decade from 2014 to 2024 (up ~125%) as the opportunity set did not scale.

Why Does This Opportunity Exist?

- WI is too small to move the needle for most funds.

- WI is engaging in a new approach with a new strategy, with two founders who are new partners.

- WI has only done one acquisition so far (Fortress).

- The current private placement transaction is required for WI to get 100% of Fortress.

Paul and Scott failed in their first attempt at this transaction, because they wanted Paul to have over 50% ownership so they could ensure they would never become the victim of a hostile takeover (like Scott with his first company). However, they learned while trying to gain regulatory approval that the regulator would require them to engage in activities that would be too costly and burdensome for such a small company (such as releasing an S-1), based on Paul owning more than 20%. So they decided to suspend the first transaction and create a new one to keep Paul’s ownership below 20%. This has taken several months. Now they feel they can’t fail twice, or else they’ll risk losing Fortress. So they have sweetened the pot sufficiently to ensure they raise the $37mm they need, hence why we will essentially receive two shares for one.

Where we are conservative in our assumptions:

- We have modeled no share repurchases but Paul will certainly repurchase stock over time, and maybe even very large percentages of the company.

- Scott and Paul have a 300mm premium “whale” in their sights.

- They believe they have the relationships there to win the deal and that timing is the key factor (they will need to do 3-4 deals first to get large enough to pull it off).

- The business is currently undermanaged as it is part of a trapped capital operation of a foreign insurer that is trying to exit Canada.

- We have not included such a large deal in our model.

Risks & Mitigants

| Risks | Mitigants |

|---|---|

| WI is unable to acquire as many companies as they had hoped. They have only acquired one so far. |

|

| Fortress brings on unprofitable business as it grows, leading to losses. Small insurers, in particular, are more at risk of adverse selection (when a broker decides to give a bad book to an insurer they don’t care about). |

|

| Western Investment acquires insurance carriers with hidden large losses that materialize after deal closure. |

|

| FX: the CAD declines against the USD, decreasing our IRR. |

|

Investment Case: BVPS Growth & ROE Formula

As at other high quality insurance companies, we believe long-term value for WI will approximately track growth in book value per share. How will WI earn >25% BVPS growth? Through a combination of profitable underwriting, underwriting leverage, good investment returns and float leverage:

BVPS Growth = [Return on Underwriting x (1-Tax Rate)] x (Earned Premiums/Equity) + [Return on Float x (1- Tax Rate)] x (Float/Equity)

Western Investment’s BVPS Growth Algorithm = ~29% = [(1-92%) x (1-26%) x 2.5x] + (7.0% x (1-17.5%) x 2.5x)

The variables in the above algorithm vary from year to year. The above is an estimate as to the average.

Endnotes

i P/B multiples for insurers around the world tend to be highly correlated with ROE. We ended the measurement period in 1997, before the stock market bubble that burst in 1999. The stock was up dramatically more through 1999.

ii Fortress is able to get seven rated reinsurance partners even though they’re only around $30mm in GWP right now. The reason is that the large insurers have all but stopped using reinsurance. The large primary insurers have essentially cut the reinsurers out, because they want to keep all the premiums to themselves. This has starved the reinsurers for premium. The largest reinsurer in Canada, Hanover Re, earns only $1bn in premium (vs the large insurers like Intact earnings $15bn). Thus the reinsurers are happy to support up and coming insurance companies like Fortress who will need steady quota share for years to come.