Fundamentals:

Value Investment (Long Term)

Highlight the irrationality of the market– (a disparity between the intrinsic value of the stock with it’s stock price)

- Buy when the value of the stock price is lower than the intrinsic value

- Sell when the value of the stock way is higher than the intrinsic value

Intrinsic value: Value that is justified by the company’s assets, earnings, dividends and definite prospects

- Consider Margin of Safety — Only invest when the gap between the stock price and your estimate of value is really large (>20%)

- Anticipate future earnings position using broad pattern of price fluctuations that is likely for the security.

Book Value (total assets-total liabilities) > Market Value (current market price*company’s outstanding shares) means market has lost confidence in the stock to generate cash flow and profit.

Value investors often like to seek out companies in this category in hopes that the market perception turns out to be incorrect.

Market Value > Book Value means the market assigns a higher value to the company due to the earnings power of the company’s assets.

Nearly all consistently profitable companies will have market values greater than book values.

Price to Book Ratio (P/B Ratio):

- Market Price/Book Value Per Share

- Book Value per Share = (Total Assets – Total Liabilities) / Number of Shares Outstanding

- Market Price/((Total Assets – Total Liabilities) / Number of Shares Outstanding)

Portfolio Strategies:

Portfolio for Defensive Stocks Strategy:

Defensive grade (Well-Established) stock: Low Risk

Criteria are as follows:

- The company must generate a minimum of $500 million in sales.

- The company’s current assets should be at least twice the amount of its current liabilities.

- The long-term debt that the company has should not exceed its net current assets.

- The company should have some earnings for the common stock each year for the past 10 consecutive years.

- The company should have a record of continuous payment on its dividends for at least 20 years.

- A minimum increase of at least one third should be evident in its per share earnings over the past 10 years.

- The current price of the stock should not be more than 15 times the company’s average earnings.

- The current price also should not be more than 1.5 times the book value.

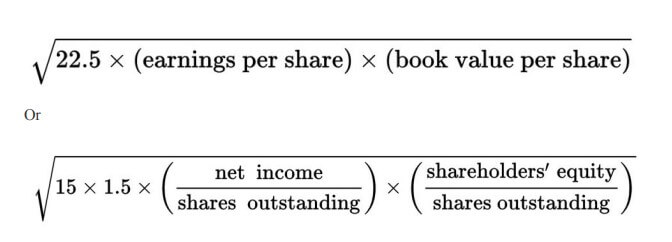

Must also satisfy Graham Number: calculates the ideal price of a defensive grade stock

Recommended to have a portfolio of 10 to 30 stocks.

Portfolio for Enterprising Grade Stocks:

Enterprising Grade Stocks: Medium Risk (Will be less established, thus requires a more careful selection and verification process. Must be tracked regularly)

Relatively safe enterprising stock, the company must fulfill these requirements:

- The current assets must be at least 1.5 times the current liabilities.

- The amount of debt cannot exceed 110% of the current net assets.

- It must show evidence of earnings stability; meaning there should be no deficit reporter in the last five years.

- The company must also have a record of dividend payments. Because enterprising stocks are necessarily less established, it does not have to be as strong as with a defensive stock. However, there must be some current dividend.

- It must also show signs of growth in earnings. This criterion is fulfilled if the previous year’s earnings are higher than its earnings five years prior.

- The price of the stock must be less than 120% of the net tangible assets.

Investors should have a diversified portfolio of at least 20 stocks.

Portfolio for NCAV Stocks Strategy:

NCAV (Net Current Asset Value): High Risk Grade stocks (Smaller, emerging companies that show a lot of potential but do not yet have an extensive record to ensure profitability)

- Eliminate stocks which have reported net losses at any point in the past year

- Price of the stock should be lower than the company’s net current assets.

- (Current Assets-Total Liabilities)/Shares Outstanding > .67*Share Price

Recommended to have a very diversified portfolio of at least 30 stocks.

Circumstantial Strategy:

Very risky (if used alone). Look special situations such as:

- Breakup of holding companies

- Arbitrage Operations

- Companies involved in complicated legal proceedings so that prices are uncharacteristically low

- Acquisitions of smaller companies by larger ones

Essentially, this strategy looks at the company’s current situation rather than simply its finances to predict the future success or decline of its stock.

Should be used in conjunction with one of the above strategies since on their own these special situations are too speculative to be useful predictors of future results. This combined use with other strategies is also advisable because investors looking to use this one should already be quite familiar with the other four before attempting something so complicated and high-risk.

Intrinsic Value Calculation:

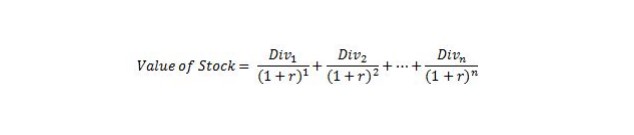

Dividend Discount Model

When figuring out a stock’s intrinsic value, cash is king. Many models that calculate the fundamental value of a security factor in variables largely pertaining to cash: dividends and future cash flows, as well as utilize the time value of money. One model popularly used for finding a company’s intrinsic value is the dividend discount model. The basic DDM is:

Where:

- Div = Dividends expected in one period

- r = Required rate of return

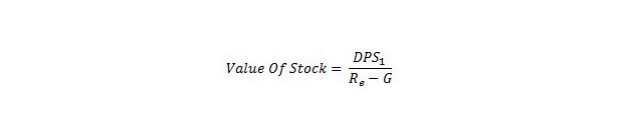

One variety of this model is the Gordon Growth Model, which assumes the company in consideration is within a steady state – that is, with growing dividends in perpetuity. It is expressed as the following:

Where:

- DPS1 = Expected dividends one year from the present

- R = Required rate of return for equity investors

- G = Annual growth rate in dividends in perpetuity

As the name implies, it accounts for the dividends that a company pays out to shareholders which reflect on the company’s ability to generate cash flows. There are multiple variations of this model, each of which factor in different variables depending on what assumptions you wish to include. Despite its very basic and optimistic in its assumptions, the Gordon Growth model has its merits when applied to the analysis of blue-chip companies and broad indices.

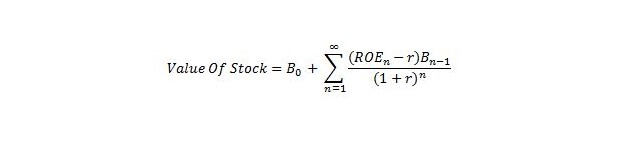

Residual Income Model

Another such method of calculating this value is the residual income model, which expressed in its simplest form is:

Where:

- B0 = Current Per-Share Book value

- Bn = Expected per-share book value of equity at n

- ROEn = Expected EPS

- r = Required rate of return on investment

If you find your eyes glazing over when looking at that formula – don’t worry, we are not going to go into further details. What is important to consider though, is how this valuation method derives the value of the stock based on the difference in earnings per share and per-share book value (in this case, the security’s residual income), to come to an intrinsic value for the stock. Essentially, the model seeks to find the intrinsic value of the stock by adding its current per-share book value with its discounted residual income (which can either lessen the book value, or increase it.)

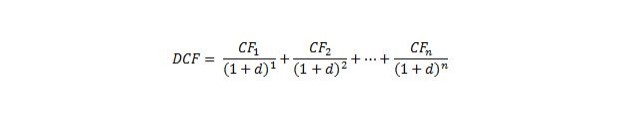

Discounted Cash Flow

Most common valuation method used in finding a stock’s fundamental value is discounted cash flow (DCF) analysis. In its simplest form, it resembles the DDM:

Where:

- CFn = Cash flows in period n.

- d = Discount rate, Weighted Average Cost of Capital (WACC)

Based on projected future cash flows.

DCF analysis looks for free cash flows – that is, cash flow where net income is added with amortization/depreciation, and subtracts changes in working capital and capital expenditures. It also utilizes WACC as a discount variable to account for the time value of money. McClure’s explanation provides an in-depth example demonstrating the complexity of this analysis, which ultimately determines the stock’s intrinsic value.

How I Find Companies:

- Subscribe to Analyst Upgrades

- Analyze implications from events

- Being aware of company changes, and press conferences